The recent collapses of Silicon Valley Bank (SVB) and Signature Bank (Signature) resulted in two of the three biggest bank collapses in U.S. history, behind the 2008 collapse of Washington Mutual. This has created uncertainty over the stability and liquidity of all banks, especially for those with over $250,000 FDIC limits in a single institution—including many small businesses needing liquidity for regular payroll.

With the level of uninsured deposits in the U.S. estimated to be over $1 trillion[1], this begs the questions: how could this happen, and how can you avoid this happening to your money?

Summary of events leading to the collapse of Silicon Valley Bank

- Silicon Valley Bank (Ticker: SIVB) was shut down by U.S. regulators on Friday due to a sudden increase in deposit outflows and a failed attempt to raise equity, resulting in a run on the bank.

- SIVB parked its excess liquidity in low-yield securities, which depreciated sharply with rising interest rates; these were sold prematurely at a loss of $1.8 billion to meet the increased cashflow needs of its depositors.

- An outflow of deposits compounded the bank's struggles due to concerns about a depreciating asset base leading to a balance sheet crunch and subsequent meltdown.

Economic Overview

Inflation has been rampant following the COVID pandemic due to unprecedented federal spending and release of liquidity into the markets paired with extreme supply chain limitations. This has caused the Federal Reserve to respond with drastic moves on interest rates.

Meanwhile, banks that have been taking long bets with some of their federal deposits are now getting crushed because they have to sell those devalued mark-to-market assets to create liquidity for the depositors. Additionally, depositors need more cash because they can't get loans at a decent interest rate—further compounding the problem.

What Happens to My Money When I Deposit It in a Bank?

When you make a deposit in a bank, it becomes a liability of the bank. And then they can do one or two things:

- purchase Treasury or other fixed-income instruments that are allowed to be purchased or

- make loans against those deposits to the public.

In 2008, we saw failure in financial institutions related to the latter with subprime mortgages. In contrast, these bank collapses highlight issues with the former—inflation negatively impacting fixed-income securities.

Banks vs. Custodians: What’s the Difference?

It’s important to understand how depositing into a bank differs from utilizing a custodian for brokerage investments. When using a custodian, that's effectively the record keeper of the assets you own. Here you control what the assets are invested in, whether stocks, bonds, mutual funds, ETFs, or similar securities that are purchased in your name. These dollars are generally not being lent out or the general liability of the custodian.

What is a Bank Collapse?

A bank collapse is when a bank becomes unable to meet its obligations to customers and other creditors. It can occur due to many internal and external reasons, including poor management, bad investments, and fraud. However, the two leading economic risks contributing to the recent bank failures are interest rate risk and liquidity risk.

Interest Rate Risk

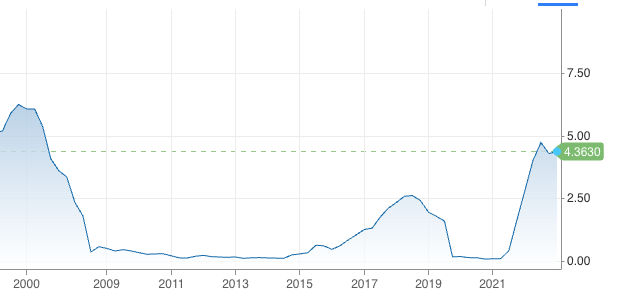

Interest rate risk is the risk that a bank faces when the rates increase rapidly within a shorter period, as it has in the U.S. since March 2022. With the Federal Reserve raising rates 450 basis points[2] within 12 months in an attempt to temper inflation, the yield on debt has made a proportionate jump. The yield on 1-year U.S. government Treasury notes jumped from less than 0.5 percent at the beginning of 2022 to a 17-year high of 5.25[3] percent in March 2023.

U.S. 1-Year Treasury Hits 17-Year High

As yields on fixed-income securities go up, their prices go down. This inverse relationship is particularly damaging to longer-term debt, such as banks who bought 5-, 10-, and 20-year notes; now all their underlying assets have a mark-to-market risk, and they are devalued on their balance sheets, leading to the second contributing risk—liquidity risk

Liquidity Risk

Liquidity risk is the risk that an asset or security cannot be bought or sold quickly enough to prevent a loss or to meet financial obligations. As the customers of SIVB were dealing with their own cash shortfalls, this pressured the bank to sell its securities portfolio at a loss of $1.8 billion and led to an attempt to raise new capital. This triggered customers to panic and rush to withdraw cash, further compounding the problem. Signature faced similar challenges. These two banks were particularly exposed to this liquidity risk as about 90 percent of their deposits were not covered by FDIC limits.

Reviewing Your Cash & Overall Risk Exposure

This particular banking crisis highlights the importance of understanding your own liquidity risks and cash flow needs as part of your comprehensive financial plan. Some of the consequences likely to result from these recent bank collapses will be a slowdown in lending. There is going to be increased scrutiny on liquidity testing, and banks are not going to be able to deploy nearly as high of a ratio of their deposits to loans. As a result, people that need access to debt and capital through lending are going to have more challenges.

It's important to consider:

- How much cash are you carrying as part of your overall financial plan?

- Where are you keeping this cash?

- If you have an excess of $250,000 that needs to be accessible cash, how can you increase FDIC protections?

- What are alternative choices to banks that are market-protected, liquid or short-term and providing competitive yield?

Where Can I Put My Cash Over $250,000 FDIC Limit?

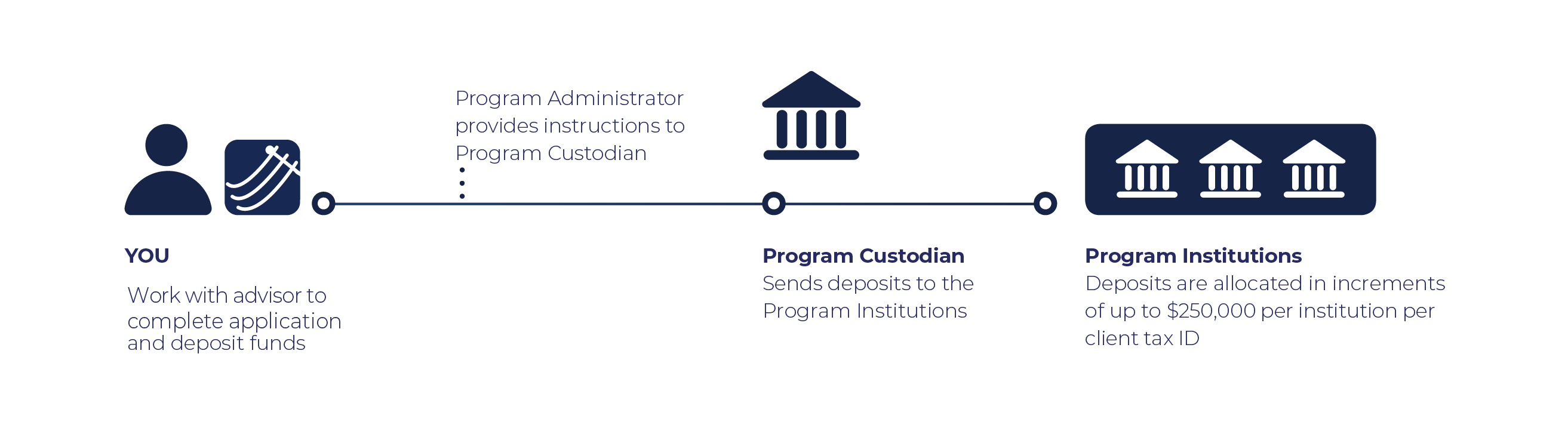

At Granite Harbor Advisors, we have access to partners that can provide competitive interest rates with FDIC insurance protection up to $25 million per tax ID. This creates a singular account experience for the investor that is then diversified utilizing a large network of banks to stay within the $250,000 per institution threshold.

For alternatives to banks utilizing custodians to maintain complete control of your underlying asset selection, we have seen a significant movement towards short-term Treasury notes as one option to consider. With yields around 4.0% right now for a time commitment of as little as four weeks, this is an entirely different environment than the near-zero rates we have experienced for the better part of the last two decades.

If you have questions about your current cash management strategy or other concerns surrounding today’s market, give us a call at 832-461-0789 or use the link below to schedule a convenient time to discuss your needs.

Data/rates/information contained herein are believed to be accurate at the time of publication and subject to change without warning or notice.

[1] https://www.businessinsider.com/signature-svb-us-banks-have-over-1-trillion-uninsured-deposits-2023-3

[2] https://www.federalreserve.gov/monetarypolicy/openmarket.htm

[3] https://cnbc.com/quotes/US1Y