Authored by: Brian W. Sak, CFP®, CLU®, ChFC®

What if the traditional approach to retirement planning—accumulate assets, shift to bonds, and draw income—misses a meaningful part of the opportunity set?

For many high-income families and business owners, retirement is not simply about replacing income. It is about sustaining a lifestyle, preserving optionality, managing taxes, and ultimately transferring wealth efficiently. Yet most portfolios rely heavily on public markets alone, often leaving gaps in protection, predictability, and long-term outcomes.

A recent study by Ernst & Young, Benefits of Integrating Insurance Products into a Retirement Plan, highlights a critical shift in thinking: incorporating insurance-based strategies alongside traditional investments can improve both retirement income and legacy outcomes under a wide range of scenarios.

This raises an important question for sophisticated investors: not whether insurance has a role, but how it should be integrated thoughtfully into a broader financial plan.

Structural Gaps in Traditional Retirement Planning

The study begins with a sobering reality. By 2030, researchers at Ernst & Young estimate a substantial shortfall between retirement savings and income needs, along with a meaningful protection gap.

Traditional portfolios—built on equities and fixed income—are effective for growth, but they are not designed to address several structural risks.

Market volatility during withdrawal years can force difficult decisions. Longevity risk introduces uncertainty around how long assets must last. Tax inefficiencies across account types can quietly erode returns. Sequence of returns risk can derail even well-constructed portfolios early in retirement. And for many families, legacy goals are addressed too late in the planning process.

Insurance products, when properly structured, address these issues differently than traditional assets. They introduce features such as guaranteed income, tax deferred accumulation, and mortality credits—elements that cannot be replicated through public markets alone.

This distinction is central. Insurance is not a replacement for investments. It is a complementary asset class with a different return profile and purpose.

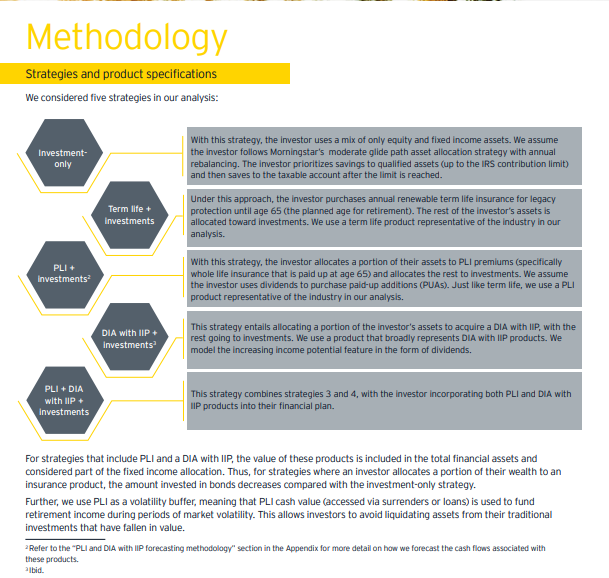

Understanding the Core Strategies Evaluated

EY’s analysis focuses on five primary approaches, ranging from investment only portfolios to fully integrated strategies.

As illustrated in the methodology diagram on page three, the key difference is not simply product selection, but how capital is allocated across growth, protection, and income generating assets.

Two insurance components are particularly important.

Permanent life insurance provides tax deferred cash value growth, death benefit protection, and the ability to access liquidity through policy loans. In the study, it also functions as a volatility buffer during market downturns, allowing investors to avoid selling depreciated assets.

Deferred income annuities with increasing income potential are designed to create a future income stream, enhanced by mortality credits and dividend like increases. These structures support longevity protection and introduce a level of predictability that traditional portfolios often lack.

These tools operate under fundamentally different economic drivers than stocks and bonds. That distinction is what creates the diversification benefit.

The Analytical Framework: A Technical Perspective

Rather than relying on simple projections, EY employs a Monte Carlo simulation framework to evaluate outcomes across 1,000 scenarios of market conditions, inflation, and interest rates.

Two primary metrics are evaluated.

After tax retirement income is measured at a 90 percent probability of success, incorporating withdrawals, annuity income, and insurance distributions. Legacy value is defined as total after tax wealth at the end of the planning horizon, including death benefits and remaining assets.

Several technical assumptions are worth noting.

Tax treatment varies by asset type, with insurance offering tax advantaged access under certain conditions. Policy loans are modeled as a liquidity source to avoid selling depreciated assets during downturns. Mortality credits enhance annuity income beyond what is typically available from traditional fixed income. Asset allocation follows a glide path approach consistent with institutional portfolio design.

This level of rigor allows for a more realistic comparison of integrated versus traditional strategies, particularly under stress scenarios.

Key Findings: Where Insurance Changes the Outcome

Permanent Life Insurance Improves Long Term Efficiency

One of the most consistent findings is that portfolios incorporating permanent life insurance outperform both investment only and term insurance strategies in terms of combined income and legacy outcomes.

As shown in the results table on page six, even modest allocations to permanent life insurance improved projected retirement income while meaningfully increasing legacy value relative to investment only portfolios.

This outcome is driven by tax deferred accumulation, tax efficient access to cash value, reduced need to liquidate investments during downturns, and the leverage created by the death benefit.

Term insurance, by contrast, provides protection but does not contribute to long term capital efficiency.

Deferred Income Annuities Maximize Retirement Income

When the objective shifts toward income, deferred income annuities demonstrate a clear advantage.

According to the analysis on page seven, strategies incorporating these annuities generated higher retirement income than all other approaches.

This is largely due to mortality credits, structured income streams that reduce reliance on portfolio withdrawals, and a meaningful reduction in sequence of returns risk.

However, this benefit comes with a tradeoff. Because annuities convert assets into income streams, they typically reduce liquid legacy value relative to other strategies.

Integrated Strategies Offer the Most Balanced Outcome

The most compelling insight emerges when both insurance components are used together.

Integrated strategies that combine permanent life insurance and annuities with traditional investments produced more efficient outcomes than investment only portfolios across both key metrics.

The chart on page nine illustrates this clearly. Allocations can be adjusted along a spectrum, increasing income, enhancing legacy, or balancing both objectives depending on the client’s priorities.

This flexibility is critical. It allows planning to align with real life goals rather than forcing unnecessary tradeoffs.

Addressing the Fiduciary Tension Around Insurance Recommendations

Despite the growing body of evidence supporting integrated strategies, there remains a practical challenge within the advisory industry. Many fee only advisors and fiduciaries hesitate to recommend insurance-based solutions, not because the strategies lack merit, but because of how those products are compensated.

This creates a subtle but meaningful tension.

Fee-only models are designed to reduce conflicts by aligning compensation with assets under management. However, insurance products are typically structured with commissions rather than advisory fees. As a result, some advisors may avoid these solutions altogether, even when they may improve client outcomes, simply because they fall outside of the advisor’s compensation framework.

This raises an important question. Is the client being presented with every viable solution, or only those that fit within a specific fee structure?

At Granite Harbor Advisors, we believe that fiduciary responsibility is not defined by how compensation is received, but by the integrity and completeness of the advice itself.

There are situations where insurance strategies, whether permanent life insurance, annuities, or other structured solutions—can play a meaningful role in improving retirement income, managing risk, or enhancing legacy outcomes. Ignoring those tools entirely would limit the scope of planning.

At the same time, we recognize that compensation structures can introduce potential conflicts. Rather than avoiding that reality, we address it directly and transparently.

When insurance solutions are part of a recommendation, the rationale is clearly explained within the broader financial plan. Compensation structures are fully disclosed in advance. Alternative approaches are presented for comparison so that tradeoffs are understood in context.

This approach places the decision where it belongs—with the client.

By presenting a complete set of solutions, rather than a curated subset based on compensation models, clients are better equipped to make informed decisions that reflect their priorities, not industry conventions. In practice, this leads to more thoughtful outcomes and reinforces trust in the planning process.

Optimal Allocation: Not Maximum, But Intentional

One of the more nuanced conclusions is that more insurance is not always better.

The study suggests that allocating between 10 and 30 percent of savings to permanent life insurance and up to 30 percent of retirement assets to annuities often produces favorable outcomes.

Beyond those levels, diminishing returns may occur, particularly if too much capital is removed from growth assets.

This reinforces an important planning principle. Integration requires balance. Insurance should be sized intentionally within the broader portfolio, not layered on without coordination.

Why This Matters for High-Net-Worth Families

For affluent investors, the implications extend beyond incremental returns.

A properly integrated plan can address multiple concerns simultaneously. It can create more predictable income without overreliance on market performance. It can improve tax efficiency across accumulation and distribution phases. It can preserve family wealth through enhanced legacy structures. And it can reduce stress during periods of market volatility by providing alternative liquidity sources.

Perhaps most importantly, it introduces a level of coordination that is often missing. Investments, insurance, and estate planning are no longer managed in isolation, but as components of a unified strategy.

The Role of Planning and Coordination

While the findings are compelling, execution is where complexity emerges.

Insurance products require careful structuring. Tax treatment depends on proper design. Income strategies must align with spending needs, risk tolerance, and time horizon.

This is where a team-based approach becomes essential.

At Granite Harbor Advisors, this type of integration reflects how we approach planning. Public and private investments are evaluated alongside insurance strategies. Tax implications are considered at every stage. Estate objectives are incorporated early, not addressed later. Decisions are made within the context of the entire balance sheet.

This level of coordination allows strategies like those outlined in the EY study to be implemented thoughtfully and appropriately.

A More Complete Definition of Retirement Planning

The traditional definition of retirement planning is evolving.

It is no longer limited to accumulating a portfolio and drawing it down over time. Instead, it is about constructing a financial structure that can support income, manage uncertainty, and preserve wealth across generations.

Insurance, when viewed through this lens, becomes less of a product decision and more of a planning tool.

The question is not whether it belongs in the plan. It is how it can be used to improve outcomes in a way that aligns with your goals, your values, and your long-term vision.

For many families, that shift in perspective is where more effective planning begins.

Disclosure: Granite Harbor Advisors, its directors, officers, and affiliates are not affiliated with Ernst & Young. Opinions on the study referenced herein are our own. The study was based on a number of financial assumptions that are not guaranteed to occur. Please consult with qualified tax, legal and financial professionals for proper allocations suited to your individual circumstances.